Financial Knowledge is power—especially when it comes to managing your money. When you understand how, when, and where you spend, even small adjustments can lead to meaningful financial improvements.

On average, people spend almost all of what they earn, leaving very little room for savings. Add rising living costs and debt into the equation, and it becomes clear why many struggle to stay financially secure. Smarter spending habits can help you break this cycle—allowing you to reduce debt, grow savings, and still maintain a lifestyle you enjoy.

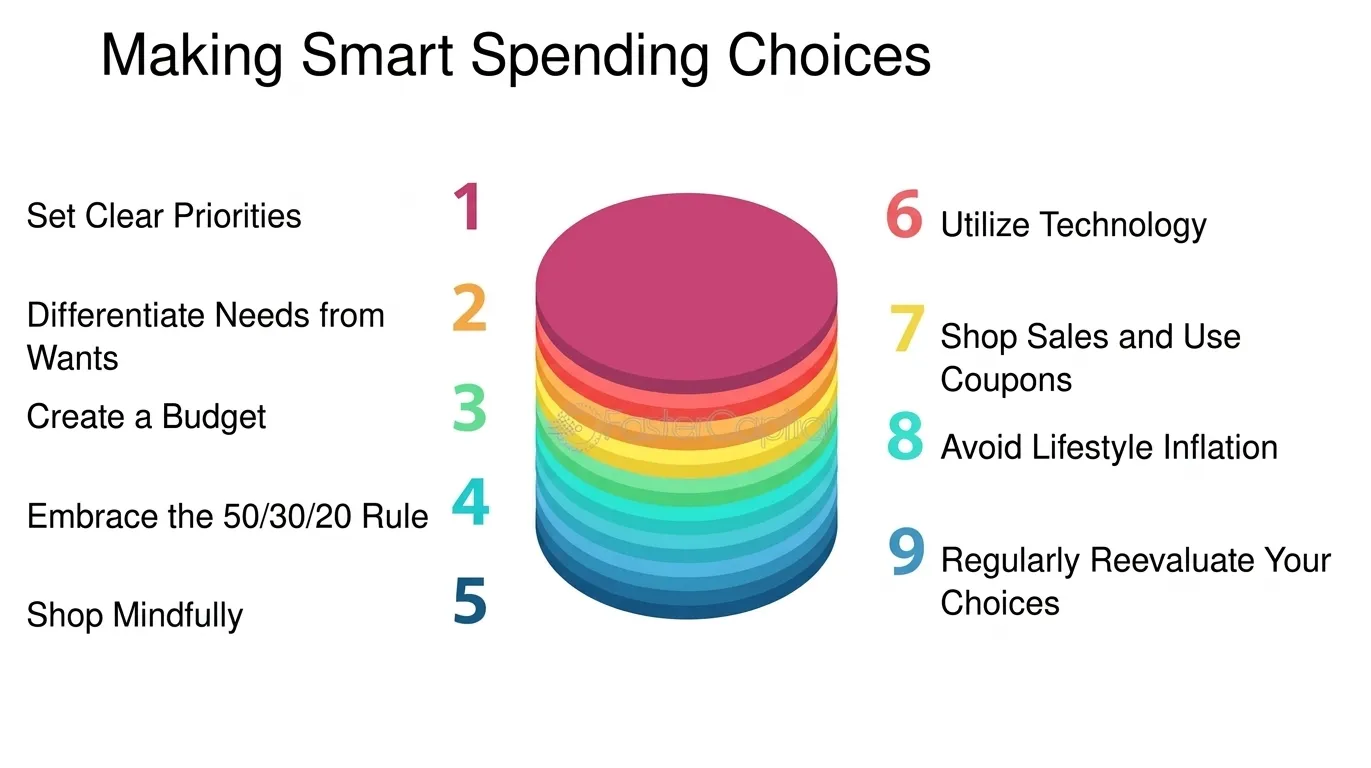

Why Good Spending Habits Matter

Uncontrolled spending doesn’t always look dramatic. It often appears in everyday situations: grabbing an extra item at checkout, ordering takeout when there’s food at home, or making impulse purchases online.

These small decisions may feel insignificant in the moment, but over time, they add up. When combined with credit card use, they can easily lead to overspending and increasing debt.

The goal isn’t to eliminate all spending—it’s to spend intentionally. You should still be able to enjoy treats, dine out occasionally, and buy things you want, as long as it fits within a controlled plan.

6 Bad Spending Habits to Watch Out For

1. Daily Coffee Runs

For many people, buying coffee has become a daily routine rather than an occasional treat. While each purchase may seem small, the cumulative cost over weeks and months can be surprisingly high.

2. Eating Out Too Frequently

Convenience often leads to overspending. Regularly buying lunch, dinner, or takeout not only increases expenses but can also result in wasted groceries at home.

3. Late Credit Card Payments

Missing payment deadlines leads to late fees and sometimes higher interest rates. These avoidable costs can quickly add up if the habit continues.

4. Choosing Brand-Name Groceries

Brand loyalty can be expensive. In many cases, store-brand products offer similar quality at a lower price, making them a smarter choice for everyday shopping.

5. Impulse Online Shopping

Online shopping platforms are designed to encourage quick decisions. Limited-time offers and easy checkout options make it tempting to buy things you don’t really need.

6. Paying for Unused Services

Subscriptions, memberships, or plans you rarely use can quietly drain your finances. Whether it’s a gym membership or a streaming service, unused services are essentially wasted money.

Individually, these habits might cost only a few dollars. But together, they can add up to hundreds—or even thousands—over time.

7 Ways to Spend Smarter

1. Understand Where Your Money Goes

Start by reviewing your spending history. Categorize expenses like groceries, transportation, entertainment, and bills. This gives you a clear picture of your financial habits and highlights areas where you may be overspending.

2. Create a Realistic Budget

Once you understand your spending patterns, create a budget that reflects your priorities. Include essentials, savings goals, and discretionary spending. A good budget doesn’t restrict you—it guides your decisions.

3. Look for Quick Wins

Identify easy ways to cut costs immediately. Cancel unused subscriptions, avoid late fees by paying on time, and reduce small daily expenses like coffee or snacks. These quick wins can free up extra cash right away.

4. Use Separate Accounts for Better Control

Consider dividing your money into different accounts: one for bills, one for savings, and one for personal spending. This structure helps you stay organized and prevents overspending in any one area.

5. Make Saving a Priority

Saving shouldn’t be an afterthought. Set aside money regularly for future goals, whether it’s an emergency fund, travel, or long-term investments. Even small, consistent contributions can grow over time.

6. Automate Your Finances

Setting up automatic payments for bills and savings can simplify your financial routine. It ensures you never miss payments and helps you stay consistent with your goals without extra effort.

7. Be Mindful with Credit Cards

Credit cards are convenient but can lead to overspending if not used carefully. Limiting usage or setting lower credit limits can help you avoid impulse purchases and reduce debt.