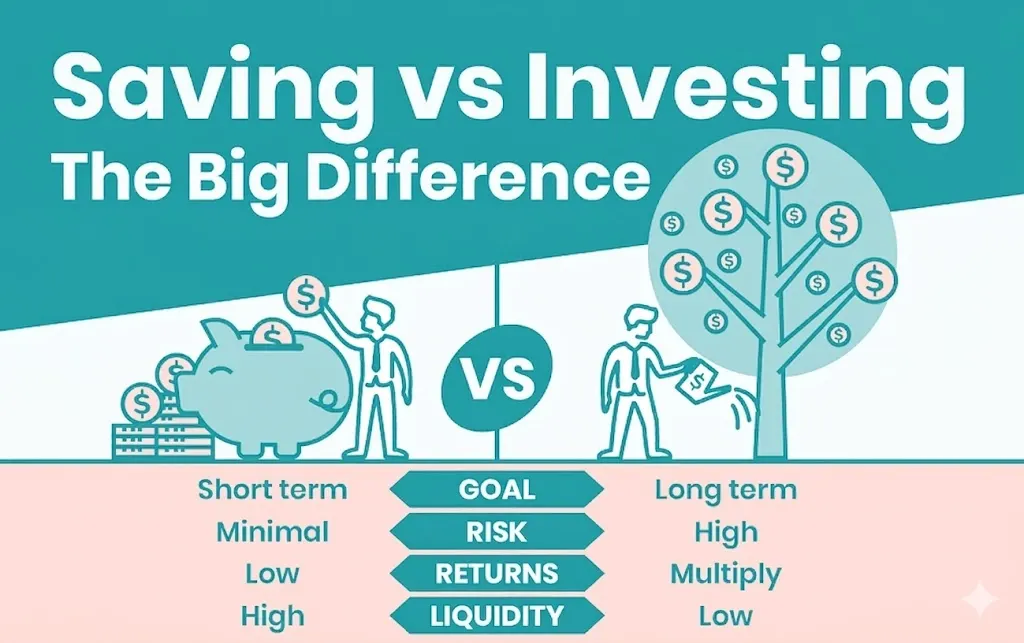

Saving is a way of storing your money until you need it. Investing, on the other hand, is about putting your money to work for you – and with investing comes more risk.

You may have wondered: “Should I save or invest?”

Here, we will explore both options to help you make an informed decision – or to determine if you might need both strategies for different purposes.

What is Saving?

Saving refers to setting aside some of your money for future use, rather than spending it immediately. You can contribute to your savings in one-off payments or regular installments. If you use an easy-access savings account, you can withdraw the money you’ve put in – plus any interest you’ve earned – whenever you need it.

- Low risk: Savings carry a lower risk of losing value. In the UK, under the Financial Services Compensation Scheme (FSCS), if a bank or building society where you hold your savings fails, you are protected up to £120,000.

- Not completely risk-free: Interest rates can rise or fall. When interest rates are low, the return you earn on your money is usually modest. The risk is that your savings may not keep up with inflation – the rate at which the prices of goods and services increase. In other words, while your money is safe in the account, its purchasing power decreases over time, meaning it will buy you less.

Saving is therefore suitable for short-term financial goals or for money that you may need quickly, as it offers security and easy access.

What is Investing?

Investing is another way to set aside money for the future, but instead of simply storing it, you put it into assets or financial instruments with the goal of making a profit over the long term.

There are different ways to invest, and most involve fees or charges. Some of the most common investment options include:

- Shares (Stocks): Buying a small portion of an individual company.

- Funds: Buying into a pre-assembled collection of investments, which are managed on your behalf by professionals.

Investing exposes you to a different type of risk, called market risk. The value of your investment can fluctuate, meaning you might get back less than you initially invested. Expected returns can also vary and are not guaranteed.

- Time horizon: Ideally, invest for 5 years or more, as longer periods give your investments more time to recover if their value temporarily falls.

- Calculated risk: While investing carries risk, taking a carefully calculated risk can allow you to earn more than you would from a savings account, potentially growing your wealth significantly over time.

Should You Save or Invest?

If you have multiple financial goals, you may want to consider saving for short-term goals and investing for long-term goals.

- Determine how much you can afford to set aside each month – creating a budget can help with this.

- Think about the purpose of the money and when you will need it.

It is helpful to split your money into several “pots,” depending on the time horizon and your financial priorities:

1. Emergency Fund

Before saving for anything else, build an emergency fund with at least 3 months’ worth of living expenses. This fund should be in a readily accessible savings account so you can access it in case of unexpected events such as job loss, health issues, or urgent repairs.

2. Short-term Goals (Next 5 Years)

If you need money in the short term, for example for a home deposit, saving is usually the best approach. Investing for less than 5 years is generally not recommended because the investment may not have enough time to recover from temporary declines in value.

3. Medium-term Goals (5–10 Years)

For money you plan to use in 5–10 years, such as for a wedding or a big trip, saving may still make sense if you prefer security. However, if you are comfortable taking some level of risk, investing in funds could provide higher returns than saving alone.

4. Long-term Goals (10+ Years)

For money you may not need for at least 10 years, such as a retirement fund, taking some investment risk can be worthwhile. Over long periods, savings lose value due to inflation, whereas investing has the potential to grow your wealth at a rate that can outpace inflation.

Key Takeaways

- Saving is best for security, short-term goals, low-risk tolerance, and money you may need immediately.

- Investing is suitable for long-term goals, higher risk tolerance, and money that you can afford to leave untouched for years to take advantage of growth and compounding.

- In many cases, a combination of both – saving for short-term needs and investing for long-term goals – provides a balanced approach to financial planning.

By understanding the differences between saving and investing, and matching your strategy to your financial goals, time horizon, and risk tolerance, you can make smarter decisions and better manage your money for the future.