Unexpected events—like a car breakdown or a leaky roof—can quickly cause financial stress. An emergency fund is money set aside specifically for such situations. Yet many people struggle to prioritize this type of savings. A 2024 survey by Bankrate found that only 44% of Americans could cover a $1,000 emergency from their savings, and 63% said inflation has reduced their ability to save.

What is an Emergency Fund?

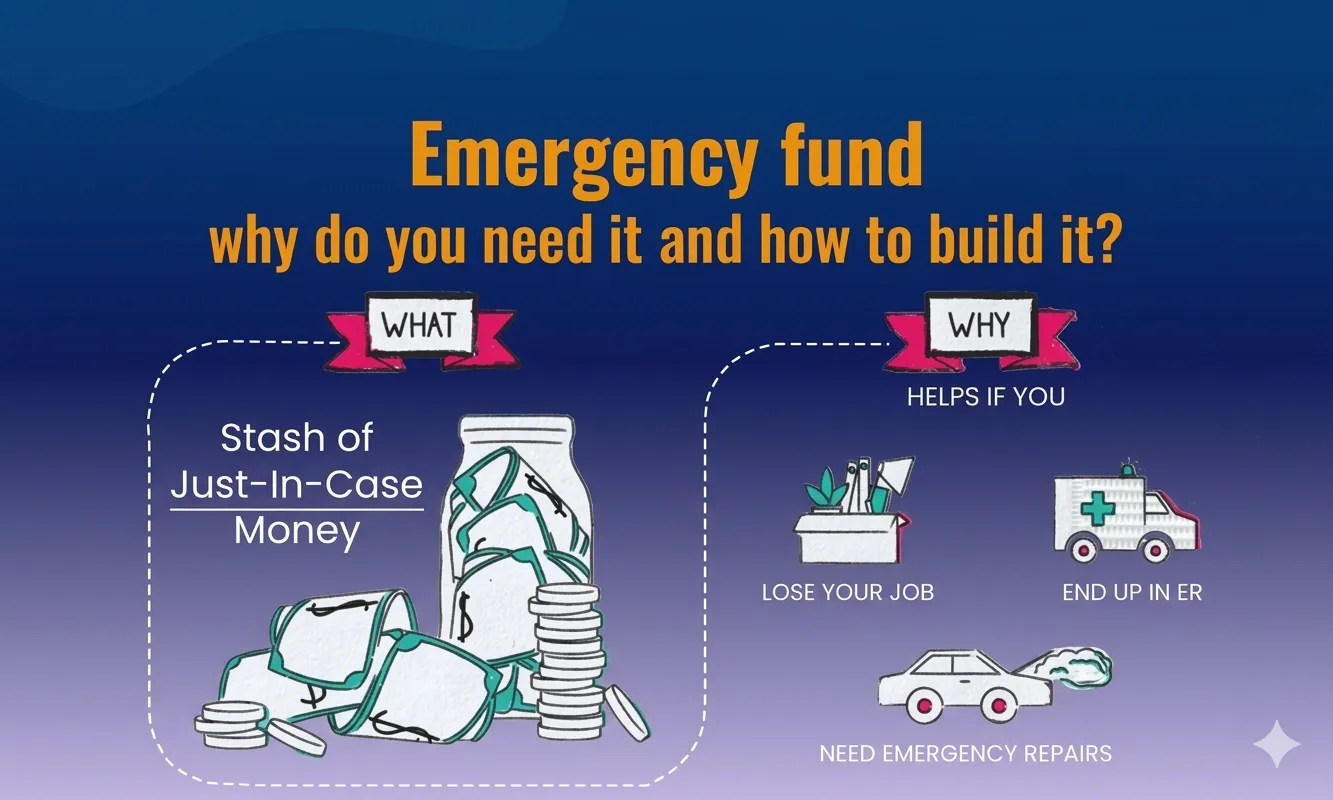

An emergency fund is money reserved for unexpected expenses, such as medical bills, home repairs, or job loss. It should be separate from your daily cash to ensure availability when needed.

Why Do You Need One?

An emergency fund prevents taking on unplanned debt or using savings intended for other goals, like retirement. Even high-income earners benefit from having a dedicated fund.

How Much Should You Save?

A common rule is to save enough to cover three to six months of expenses. The exact amount depends on your circumstances—number of dependents, dual income households, or other financial support. Single-income earners or self-employed individuals may need more.

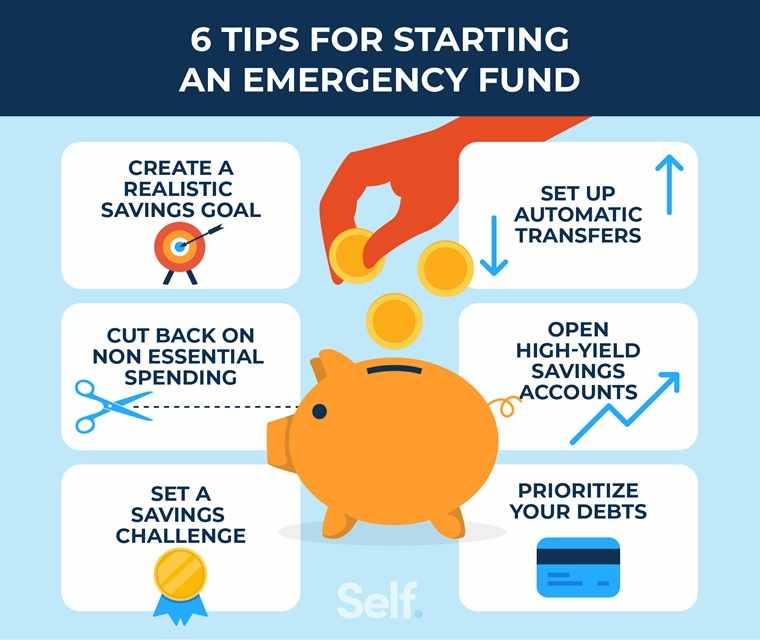

How to Set Up an Emergency Fund

- Use a safe, accessible account – A basic savings account or money market account linked to your checking account works best. Avoid investing these funds in stocks or bonds.

- Seek interest or yield – Some high-yield savings accounts offer annual returns.

- Start small – Set up automatic transfers from your paycheck until you reach your target.

- Only use it for real emergencies – Examples include car accidents, job loss, burst pipes, or large medical bills.

- Replenish after use – After an emergency, prioritize rebuilding the fund so it’s ready for the next unexpected event.

Even if you don’t need the fund for years, having this financial cushion provides peace of mind.